why web3?

All is mind. Money is mind. Yes, a figment of our imagination. I saw a llama for the first time in Bogotá, Colombia. We love animals because of their simple approach to life and innocuous tendencies. If you were to hand a llama a dollar bill, I doubt you’d be surprised if it ate it. You hand the same bill to a human, and they’d pocket it with gratitude. Money is recognized and used by homo sapiens because it is used as a store of value, a medium of exchange, and a unit of account. Various civilizations used different tools for this purpose in the past. Some used seashells, others used beads, and plenty used animal skins. Today, we use printed bills, minted coins, and bits in bank computer servers. This paper was written to reflect on what we’ve tried as a race and to open your mind to new possibilities.

A History of Money

The history of money and the economy has been slow in the grand scheme of recent humanity, but fast & innovative in the last 100 years. People have access to more information, and compounding rewards return fast when we’re talking about the language of value. Economic innovation is rooted in a long journey of trial and error. It turns out to be prohibitively challenging to create a reliable currency without a large, trusted intermediary. Without this intermediary, I can say my fur skins are worth thirty of your shells. Next week I can say they’re worth forty. Of course, game may have been harder to come by in that past week, but without a trusted standard, humans were stuck with estimates making commerce a pain. And be honest, if you didn’t know better, you’d do the same. Overvaluing your barter tender is simply the incentive of a system without standard currency.

Currency was used as early as 2000 BCE by the Shang dynasty in China. Since then, thousands of currencies sprang up in civilizations around the world. With physical currency, storing it became a challenge. Empires such as the Romans used temples to securely store excess coins. Early churches actually lent out coins to people before banks existed. Banks came about to take over this role soon after, but they weren’t as pivotal to society as they are today. Institutional banks as we know them didn’t grow rapidly until stocks and bonds were available as assets. When the Dutch East India Company was founded, investment banking became one of the best ways to generate wealth. The most lucrative business endeavors were those that colonized and exploited other nations such as India, America, and Africa. Investing was a tool to enable collective action, but it incentivized greed and the removal of human morals for more wealth. Banks subsequently became some of the most powerful institutions in the world. One of the largest banks of today, JP Morgan & Co, ended up balancing the market after a financial panic in 1907. After seeing the power of private banks, the Fed was planned and founded in 1913. This started the modern era of banking.

The Great Depression led to the New Deal which, despite its inherent racism, helped stabilize the United States’ financial ecosystem. The Federal Deposit Insurance Corporation (FDIC), which insured bank deposits, made banking far more comfortable for the average consumer. Commercial banking boomed. By then, the United States had become the world’s financial power. This was because several nations needed to borrow from the US for the first world war amongst other expenses. The US standard was fortified with the Bretton Woods agreement that set USD exchange rates for Canada, western Europe, Australia, and Japan. USD was then convertible to gold, but this would end in 1971 when currencies were balanced relative to one another via floating exchange rates. At this point in time, currency was no longer backed by anything hard to find & produce like gold ingots. It was backed by a trusted intermediary.

We’ll dive into decentralization later, but at this point in history, we can see a clear pattern of centralization of wealth. Banks worked closely with the governments that stabilized currency value and enabled them to conduct business with loans and insurance. From colonial monarchies to powerful democracies, banks were incentivized to work with wealthy governments that could provide them with security. However, with this came a consolidation of wealth amongst governments and the wealthy; a pattern that solidified with the new age of digital banking.

The Internet’s ancestor, ARPANET, went live in 1969. This was the birth of the Internet and the light-speed transfer of information we now know and enjoy today. As computers proliferated, particularly with the boom of PC’s in the 1980s, it became much easier for banks to make transactions digitally. This way, rather than accounting for physical bills, the financial ecosystem had easy-to-manage bits on computer servers to manage. IBM brought the concept of magnetic strip cards to the market in the 1960s, enabling a fully digital, bank-backed consumer experience. Today around 46% of banking activity is digital-only.

Enter Crypto

This makes way for digital-native money: cryptocurrencies. Here are the main differences between digital cash and cryptocurrencies: Digital currency supply is controlled by financial institutions (like the Fed); cryptocurrencies can be minted by anyone with the proper know-how and an algorithm determines when new coins should stop being minted The transfer of cryptocurrency requires no intermediary; digital cash is transferred and accounted for by a central party like a bank Though both require the internet, digital currencies are typically managed by central computer servers; whereas cryptocurrencies are managed by decentralized networks

Here’s some vocabulary that will help us from here:

Blockchain - An unchangeable list of data (such as a list of transactions) formed by consensus algorithms across several computers Bitcoin - The first cryptocurrency and the first mainstream implementation of a blockchain Crypto - Short for cryptography; represents the entire suite of tools and technology built with sophisticated cryptographic schemas Cryptography - etymologically means “secret writing.” A way of using mathematics to obfuscate, prove, and recover messages Cryptocurrency - A currency created and managed by a decentralized network using blockchain and cryptography DAO - A decentralized autonomous organization. These organizations operate entirely on voting consensus and cannot (should not) be controlled by a single group or person. Think cooperatives that run on smart contracts Decentralization - The process of removing centralized authorities and facilitating the same processes amongst several participants; think a swarm of bees vs. a single wasp DeFi - the construction of financial systems that do not need 3rd party intermediaries; typically built with decentralized technologies like blockchains Ethereum - The first blockchain that enabled smart contracts: the technology that enabled tokens, NFTs, and web3 On-chain / Off-chain - Computations, transactions, or actions that occur “on” a blockchain or on other computers that are not a part of the blockchain’s virtual machine Smart Contract - A program that is hosted by a blockchain; executes no matter what and can be used to create DeFi primitives amongst a theoretically infinite number of other routines that require trust Token - A currency that is created on a blockchain like a cryptocurrency. The key difference is that cryptocurrencies are a part of a blockchain’s protocol, whereas tokens are created by smart contracts Web3 - The version of the internet where users can transfer value along with reading and writing information. The accounting of value is managed by decentralized technologies like blockchains

In 2009, the Bitcoin blockchain went live, becoming the world’s first cryptocurrency. The big innovation of Bitcoin was simple: create a currency that required no intermediary like a government or a bank. Currency has never worked like this until now. Though banks have a history of discrimination and malpractice, I want to make it clear that this is not an essay against banks. In fact, I think banks are critical to the success of decentralized currencies. Their participation is critical to the connection of blockchain assets to real-world assets. MakerDAO, a decentralized stablecoin protocol, even worked with Huntingdon Valley Bank in Philadelphia to loan $100M in stablecoin assets (to my knowledge, this deal fell through; great proof of concept though!). However, the innovation of a currency where the individual is the full owner and custodian of their assets has not happened yet. Smart contract enabled blockchains are special in that they add more functionality beneath what a currency can do. Not only do users outright own their assets (rather than owning through a bank where sometimes it costs money to not have enough money), they can use their assets to perform the financial responsibilities of what a bank, currency exchange, insurance agency, etc. would do. We’ll go over examples later, but it’s imperative to fully understand the open nature of a smart contract-enabled blockchain. Any person with an internet connection can deploy a smart contract to the blockchain. This is an amazing innovation but has resulted in billions of dollars lost due to hacks, scams, and the overall unintuitive nature of blockchains. Though billions have been lost, the technology is maturing at a fast rate and is getting closer to full market readiness every day. All great things take time.

We mentioned MakerDAO earlier. Their DAI stablecoin was one of the first tokens created on Ethereum. The core functionality of MakerDAO is to “make” DAI by converting loan collateral into tokens pegged to the US Dollar (i.e. a stablecoin). MakerDAO works through smart contracts. You can even take a look at the code here if that’s your thing.

Tokens on smart contracts are standardized by the EIP20 specification (EIP stands for Ethereum Improvement Proposal). In this specification, tokens are laid out to include basic data and functionality like a token name, symbol, a function for transferring the token, a function for finding the token balance of a particular user, amongst others. You can see the full specification here, but there are several other specifications that allow multiple smart contracts to communicate with one another in a safe, intuitive way.

This standardization makes way for DeFi. It is the use of smart contracts to build the logic for decentralized financial institutions. Here are some of my favorite examples:

Uniswap is a decentralized currency exchange. It launched in 2018 and is considered the first automated market maker on the Ethereum blockchain. An automated market maker is a DeFi primitive for incentivizing users to provide two-sided liquidity that helps a decentralized exchange (DEX) work. Let’s say I want to swap one token for another. Rather than using a centralized exchange such as Coinbase or Binance, I can use a decentralized exchange like Uniswap. Uniswap enables everyday users to provide liquidity and earn passive income on swap fees rather than centralized intermediaries. This is a big part of why I’m excited about DeFi; it allows the economy to be run by the people.

AAVE (not to be confused with African American Vernacular English; this AAVE means “ghost” in Swedish) is a decentralized lending and borrowing platform. On AAVE, users can lend their crypto tokens in exchange for a piece of the borrowing fees. Other users can use collateral to borrow from the lending users.

Nexus Mutual is an on-chain insurance service that insures blockchain protocols. Members of the Nexus Mutual DAO can buy insurance coverage for assets like protocol tokens. Nexus Mutual has risk assessors who verify smart contract code and make sure that it is secure. They also have claims assessors who decide whether or not to accept a claim made by a coverage owner.

These three amongst several others are the earliest decentralized finance protocols, but I want to highlight that all three protocols are not controlled by a small group of people. They are controlled by DAOs. Multiple people from across the world. In fact, my alma mater, North Carolina A&T, has a crypto club where college students are voting on decisions that Uniswap is making regarding their protocol. Not wolves of Wall Street, HBCU students. I hope the point here is clear. Money and finance as we know it has evolved past the need for centralized authorities to maintain its use as a store of value, a medium of exchange, and a unit of account.

The Separation of Money and State

I would like to preface this section by saying that there is nothing inherently wrong with banks. They are our best effort at providing a stable economy and have provided countless people with positive opportunities.

I have sharp criticisms about the formation of the United States, but I am grateful for the innovative values that were made standard here. The country was founded on many core principles, one of them being the separation of church and state. In the Constitution, it is stated that “Congress shall make no law respecting an establishment of religion.” This was a revolutionary idea in the western world that set the United States up to be the melting pot we know it to be today. With the freedom to choose your religion or faith, people from all over the world saw the opportunity to move to the United States and live in a more free environment. Creating this barrier gave the government a more focused role that involved providing law and order and defining the rules of the nation.

The next revolutionary movement involves the separation of money and state. Just like the empires of old, nations today have intertwined their power over the law and their power over the economy. Establishments like the Fed and central banks were made to be separate from the government, but they are not separate to the degree that Jefferson envisioned the church and state to be. Erik Vorhees was the first person I heard mention this philosophy. In the linked article, it is mentioned that the separation of money and state is arguably just as / more important than the separation of church and state. I agree. As we’ve seen before, governments only had power over currency to make it so that currency was trustworthy. Now that we don’t need them, why would we keep allowing a small group of people to dictate what happens to the money that everyone uses?

Martin Luther was excommunicated from the Roman Catholic Church for denying the opinion that people had to go through priests to receive the grace of God & Christ. The idea seemed ridiculous at the time, but it’s common sense to lots of people today. After he translated the Bible to German, people started reading it for themselves and experiencing God directly. Knowledge of money can have the same effects on people; it certainly did for me. As a young engineering student, I never dove into the details of finance. I had horrible spending habits and saw money as something to spend, not something to leverage. When I would learn about DeFi, I naturally had to learn about finance. I grew more educated about what money is and what it can be used for. Podcasts like Earn Your Leisure helped tremendously, too. I now have an investment-based mindset rather than a consumer mindset. I have a financial plan and am aware of what I can do with a good credit score and an entrepreneurial outlook. It was freeing to finally know money; something I thought I had “known” since using that $5 bill to get Hot Krunchy Kurls and candy at the corner store several years ago.

“How come there are no corner stores in white communities?” is what I would ask myself when driving through places like Naperville, IL. It took me time to learn that communities were designed this way in large thanks to institutions like banks. When you can control where loans go, you control where people and businesses end up.

My father is the most incredible man I know. Thinking about his origins makes me marvel at his poised, friendly demeanor today. Growing up on the west side of Chicago, despite his parents having successful business careers, he was stopped, frisked, and abused by the police regularly. One would ask why a successful family wouldn’t move to a better area, but being black in America made it orders of magnitude more difficult to do so. It’s often referred to as a joke when people mention “making it out the hood,” but there’s a grim reality behind that statement that most people don’t appreciate or even think about. Banks would refuse loans to black people who wanted to move to better communities with better resources and schools. Places that didn’t have corner stores and fast food, but grocery stores with real food. Food availability & consumption is one of the best predictors of crime and literacy rates. Healthy people make healthy decisions. Take healthy food away, and you can corrupt an entire group of people. Despite the hardships, many of these families could afford to move to better places. They just couldn’t get the mortgage to do so. The practice of redlining was an effort by the banks to mitigate loan risks, but it ended up being another source of wealth division amongst people based on the color of their skin. This is just what happens when emotional human beings have control over resources. Despite countless forms of malpractice, black communities still haven’t even gotten a formal apology from banks or the government.

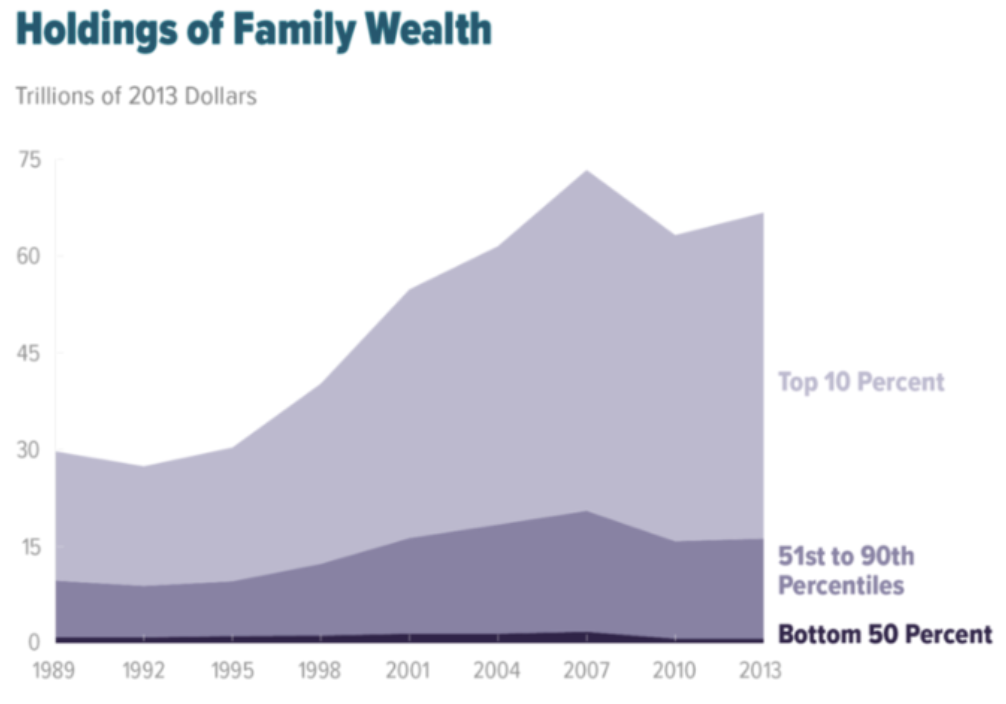

Think about how different the world would be today if we didn’t have to trust powerful people to run the economy. Just like how the world can reflect on how restricting it must have been to receive spirituality from a flawed priest, we can imagine the future generations thinking of how restricting it must be to have to be born into financial freedom. It’s why millions see the “Land of the Free” as a dull joke. A farce. This isn’t a matter of whether we want to or not; we must separate money and state. If we don’t, we’ll keep exacerbating this harsh reality in the US:

This graph simply shows the incentive people with power have. Let us not wait until these people are satiated. Let us not trust people. Let’s trust the most trustable thing in the world: mathematics.

“Nothing discloses real character like the use of power” - Robert G. Ingersoll

Ultra Sound Money

Bitcoin is called “digital gold” because there will be a time when Bitcoin miners won’t be able to feasibly mine new Bitcoin. The difficulty to mine it will just be too high to make a return on the investment. In fact, Bitcoin is more securely scarce than gold because the universe’s supply of gold is theoretically infinite, whereas Bitcoin is a finite program. This is what got people calling Bitcoin “sound money.” It is a finite, scarce resource that is more natural than the rather sporadic printing and interest rate manipulation used today. It’s a great effort to remove inflation from currency since inflation, in reality, shouldn’t exist. However, large corporations and nation states have invested millions into mining Bitcoin and claiming a large share of the supply. Bitcoin can be mined very efficiently with specialized (and expensive) computers called Application-Specific Integrated Circuits (ASICs). When all the Bitcoin is mined, it’s likely that a large portion of it will be held by those who were already wealthy to begin with. Though Bitcoin is more decentralized than a central bank, it still isn’t something we can rely on for the true separation of money and state.

The term ultra sound money comes from what people started calling Ethereum, especially after the London hardfork where EIP-1559 was introduced. EIP-1559 burns a base amount of the ether currency after every transaction. According to ultrasound.money, as of right now 9,444.84 ether has been burned since the hard fork. That is equivalent to $15,312,682.97 that no longer exists in order to make the currency anti-inflationary. Though ether as a currency is not deflationary, it’s becoming inflation-resistant. Let’s remember, this resistance is not managed by human beings with an interest rate lever, but an algorithm that works the same for everyone regardless of their gender, race, credit score, or last name.

Remember how ASICS can be bought to mine Bitcoin more efficiently? Ethereum runs differently and is resistant to strategies like this. When Ethereum ran blockchain consensus on Proof-of-Work (what the Bitcoin blockchain uses for consensus), the mining challenge was not just computationally intensive like Bitcoin, but it was also memory intensive. Computation is a computer’s ability to crunch problems like multiplying 7382992735 by 8574348929. Memory is a computer’s ability to temporarily store and access a value like 115,792,089,237,316,195,423,570,985,008,687,907,853,269,984,665,640,564,039,457,584,007,913,129,639,935 (the maximum number of a 256-bit / 32-byte value). Memory takes more time and energy than compute because computation and memory are done on two different computer architectures. One uses logic gates and arithmetic units to crunch numbers while the other uses transistors and capacitors to store and retrieve values. This makes it hard to make specialized computers for Ethereum mining because it would be more cost-efficient to roll with a common architecture that plenty of people use anyways. Now, Ethereum runs on Proof-of-Stake which lowers the technical complexity by a landslide and uses cryptoeconomics to ensure that blocks in the blockchain are valid and accurate (while using less than 1% of the energy Proof-of-Work consumed). Proof-of-Stake was also activated in the London hard fork along with EIP-1559.

This is where we get to the answer of “why web3?” web3 is this version of the Internet where we can own assets thanks to blockchain & distributed ledger technology. But the beauty of it lies in its collective, decentralized culture. These upgrades were made to improve the technology for everyone, including the environment, not just a few rich people. EIP 1559 does burn a bit of currency after you make a transaction, but it does it for the greater good of everyone else in the network. Yes, miners make less money with proof-of-stake, but the collective community decided that using less electricity was more important. The human collective should be the governor of money, not the powerful few. This is the attitude that web3 has and looks to be our best shot at creating an equitable, trustless monetary policy.

I couldn’t mention web3 without mentioning non-fungible tokens (NFTs). NFTs have a horrendous reputation, but their potential is astounding. Along with decentralized currencies, NFTs allow us to have decentralized assets that represent unique and/or real-world items. One of my favorite use cases for NFTs are real estate NFTs where homes can be exchanged as easily as any other digital asset. Precautions are necessary, which is why real estate has historically been done with a bank. Once again, this tech isn’t anti-bank; banks can be good. Regardless of a person’s preference, though, having the option to buy a house like an Amazon book can be a great convenience.

This is certainly not a proposal for us to move all our assets to Ethereum and call it a day. It is also not a promotion of Ethereum. There are criticisms I have regarding Ethereum, in particular its tendency to act as a bureaucracy and its low capacity for resonating with most of people in the world outside of the computer scientists. My core purpose here is to introduce a new idea of what money should be. The possibilities today are endless thanks to technology. If we can have an automated currency that nobody can control, true financial freedom for all is right at our fingertips.

Technology doesn’t solve everything, though. A major drawback of decentralized currencies is that they are only digital; meaning that physical bills and coins aren’t yet possible with these frameworks. Physical currencies are important for accessibility purposes. Another drawback is that it can be complicated to understand. A lot of what happens in web3 is spoken in a technical language that isn’t accessible to the masses. I want to help change that, but I encourage you to never fear the unknown and keep learning!

Conclusion

We made a mistake calling any period of time “The modern era.” Time is a river that flows continuously, and though we are at the end of some phases, we are just beginning new ones. New technologies are enabling us to do things we never thought were possible before like doing this money thing without a bank or government. It will take some getting used to and it will require some reflection, but one thing that we must learn is to never doubt innovation. Ultrasound money isn’t just a cool tech project. It’s a once-in-a-generation innovation. As a programmer myself, when I discovered this technology, I couldn’t keep my mouth shut. This is why I want to write and break this tech down for anyone to understand.

I want to emphasize again that this is not a diss track against banks. This is just a signal toward an innovative solution that is simply better than what we’ve been doing. I also want to emphasize that a central bank digital currency is not a panacea or even a step in the right direction. Remember, we should be headed toward a future that increases the freedom and autonomy of all human beings. Creating a central digital currency keeps power in the hands of the powerful. Many will fall for it, but the people who truly care about our posterity will support a currency system that cannot and will not be controlled. Thank you for reading!!!